NOL calculations are complicated so this illustration is

only intended to give you a general idea of how it may operate as a Roth

conversion tax strategy for a business owner. You should always consult with

your personal tax professional regarding your situation.

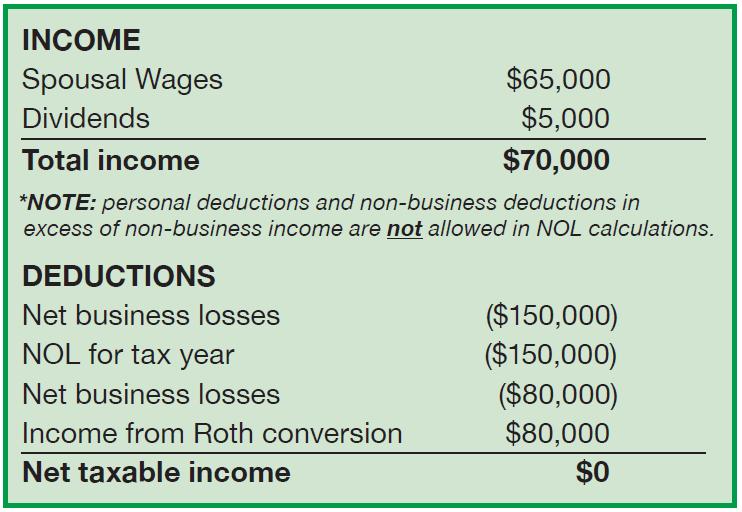

Assume a sole proprietor has $150,000 in net business losses

and $80,000 in net operating losses for the year. Assume the business owner

also has a SEP IRA with over $150,000. He then converts $80,000 of his SEP IRA

to a Roth. Because the Roth conversion is taxed as ordinary income, he uses

that Roth “income” to offset the net operating business loss:

In this example, the

owner may be able to convert $80,000 of his SEP IRA without creating taxable income.

If a company has a net operating loss, it may apply this tax relief in one of

two ways:

1) It can apply the net operating loss to its past tax payments

and receive a tax credit; or

2) It could apply the net operating loss to future income

tax payments, reducing the need to make payments in future periods. The terms of the tax relief and how it can be applied varies

by jurisdiction but usually the NOL can be applied to the past 2 or 3 years or

to future years (carry forward).